VR in 2016: Year in Review

By Mary Ermitanio

Around this time last year we were all looking forward to what we thought would be the biggest year yet for VR, when consumers would finally be able to get their hands on the major U.S. headsets. The year 2016 was indeed a major milestone in the timeline of VR, marked with a lot of experimentation, new ventures and partnerships. The VR ecosystem has grown significantly over the last year, with now over a thousand VR apps/experiences available on the Vive and Rift headsets and one million VR users per month, according to Mark Zuckerberg during a speech at Oculus Connect.

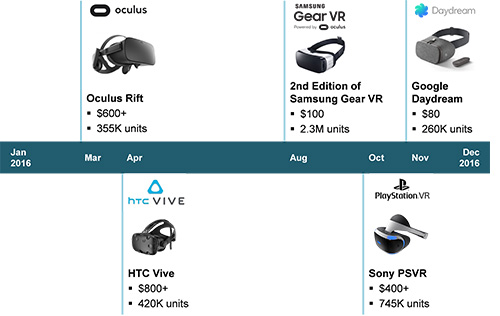

The timeline below illustrates the releases of major headsets this year and unit sales through 2016, as forecasted by SuperData Research.

AR headsets have not hit the consumer market yet, but AR headset makers, such as Microsoft and Meta, have shipped out new developer kits this past year as well. Needless to say, AR/VR is still in its nascent stages, with major hurdles to overcome. The biggest barriers to consumer adoption of VR are the need for more compelling content, especially for nongaming audiences; bulky, tethered headsets that can lead to poor user experience; and the high price points of headsets. To date, what we have seen is really just the first generation of headsets and experiences. The billions of dollars of funding being poured into the market will only accelerate the pace of development and shorten the path to mass market adoption.

Several investment funds have been formed and investment announcements made in the last year to support the growth of the AR/VR market. Here are just a few:

- The Virtual Reality Venture Capital Alliance (VRVCA) is a $12 billion fund with over 35 participating investors

- HTC announced a $100 million investment fund, alongside its Vive X accelerator program

- Facebook will invest another $250 million into VR content (in addition to the $250 million investment it has already made in content)

- IMAX announced it will invest $50 million into VR projects

- The VR Fund is an early-stage VC launched with a target amount of $50 million to invest

- COLOPL, a mobile gaming company, launched a $50 million fund for VR game projects

According to Digi-Capital, the AR/VR market saw $2.3 billion in investments in the 12 months following October 2015. While a sizeable chunk of the funding went to Magic Leap, much of the funding flowed into VR tools and solutions enabling the creation and distribution of VR content. The next wave of investments will most likely be directed towards content and applications. In a recent survey of AR/VR startup founders, tech executives and investors, content in gaming, movies/TV and live events were the top three sectors for investment in the next 12 months.

Due to the aforementioned adoption barriers, monetization of VR content hasn’t quite taken off this year. There were only two games (by L.A.-based Survios and Canada-based Cloudhead Games) that have surpassed $1 million in sales, as reported by UploadVR. Much of the paid content available are games, with price points ranging from $2 mobile experiences to $60 high-end, tethered experiences. A majority of the VR content available for free are marketing vehicles. However, the move to monetize non-gaming content has begun and will continue into the new year. For example, Fox has released The Martian VR Experience and will be charging $20 for it on PSVR and the Vive. Kygo’s VR experience, which is more interactive than the usual 360 music video, will be available for an undisclosed price. And let’s not forget, Sony had recently co-financed the first VR film slate, taking the studio’s relationship with VR beyond pure marketing.

While consumers wait for more and better content, more comfortable headsets and more accessible price points, perhaps the biggest driver of consumer awareness and acceptance of VR will be location-based experiences (LBE). I use the term broadly here to refer to both temporary and permanent physical VR installations, arcades and theme parks. Brands have used VR activations to sell products and services (see Toyota delivering a VR experience to drive car sales), improve customer experience (see Marriott’s in-room VR entertainment), and improve overall brand awareness through engaging experiences (see my post on McDonald’s activation at SXSW).

Consumers are already used to paying for experiences at theme parks, arcades and theaters. VR LBEs are the most analogous to these and can not only bring VR to the masses in a way that is curated and controlled, but can also monetize VR today. IMAX will start to pilot “VR Centers” around the world, starting in Europe. Its VR experiences, which will include the use of major movie and game IP, are said to be around 10 minutes long and will cost $7-$10. HTC recently launched the VR theme park Viveland in Taipei and also aims to bring thousands of VR arcades to consumers around the world. It launched its Vive Arcade platform, which aims to connect content creators to operators of arcades or other venues.

We now look forward to 2017. We expect lower prices and better user experiences for the next iteration of headsets. Microsoft has announced launching $300 high-end headsets with PC partners, including Acer, Asus and Lenovo. We will see improvements in VR content and experiences as technologies improve and creators learn from and respond to consumer feedback. We also look forward to more announcements around AR, including phones with capabilities to support advanced AR (such as those with Google’s Tango technology) and the first set of consumer-facing AR headsets from companies such as Meta, Microsoft, ODG, and perhaps the secretive startup Magic Leap.

back to top

PSVR: Insights Into the Pace of VR Adoption

By Jordan Pritchett

There has been a great deal of speculation and anticipation this year surrounding the rollout of virtual reality products to the mass market. Since the outset of 2016, expectations have been running extraordinarily high, and rightfully so, considering the far-reaching potential this very nascent industry brings to the table. Last month BI Intelligence Daily forecasted that global shipments of VR headsets would spike to 8.2 million in 2016 and propel the VR space to exceed $1 billion in its first year.

This is an ambitious projection to be sure, even for a game-changing technology as revolutionary as VR. Therefore, as we enter the final stretch of the holiday season and veritable peak of consumer purchasing, industry insiders have been intently examining available statistics to benchmark the industry’s growth and determine whether it is taking off at a pace that is in line with market expectations.

While the industry has undoubtedly made significant strides throughout the course of this year, its momentum thus far during the holiday season has served as a somewhat sobering reality check. SuperData recently revised its 2016 forecast, calling for under 750,000 PlayStation VR units to be sold and 261,000 Google Daydream units sold. Meanwhile, HTC Vive, Oculus Rift and Gear VR remained consistent at 420,000, 355,000 and 2.3 million, respectively.

Sony is uniquely suited for success in VR. It benefits from an existing consumer base of over 50 million PS4 owners (making the processes of upgrading to VR much easier) and a moderate price point of $399. Due to this competitive advantage, Sony currently commands the greatest portion of market share for VR, which is now estimated at 30%.

While no official numbers for 2016 have been released by Sony, the overall reception of the product has been strong. Shuhei Yoshida (Sony Interactive Entertainment Head of Worldwide Studios) underscored this point in a recent interview and noted that the company was most surprised by the duration that its users were spending inside of their headsets. Yoshida did not reveal which games were being played the most, but Sony has confirmed that Batman: Arkham VR and Job Simulator are selling best on the PlayStation Store.

PSVR’s six-month roller-coaster ride serves as an interesting case study and provides a useful lesson that will be important to remember as the industry continues to unfold. Certainly, 8.2 million headsets looks to be a bit of a stretch for VR’s debut year; however, the biggest stretch of all, at this point, would be to label VR the “biggest loser” of the holiday season. Point-blank, this is only the beginning. The best content is yet to come, the ecosystem will continue to consolidate and provide a more ubiquitous experience and at a much more affordable price. So, while industry analysts may have jumped the gun in anticipating just how quickly widespread adoption would occur, the end result has remained unchanged. VR is and will continue to disrupt the digital landscape.

back to top