From major studio M&A deals to the intensifying battle between tech and TV giants, the major events of this past year are completely transforming the face of the industry. These deals and announcements come at a time when video is more fragmented and diverse than it’s ever been.

There is greater variety in who is creating content—no longer just studios, but a whole slew of creators including digital-first studios, publishers, brands and, of course, influencers and users; in what types of content are being consumed—premium long-form and short-form, influencer, and user-generated; and where the content is consumed—cable/broadcast, streaming services, social platforms and messaging apps.

The state of video today is defined by the impact of a generational shift and strong preference for digital viewing, competitive pressures in advertising, and unprecedented consolidation and collaboration in the industry.

People are watching more video online (in more places) than ever before.

In the United States, people spend more than eight hours a week watching online video—that’s 1.5 hours more compared with last year, and two hours less than the time spent on broadcast, cable and satellite TV. Traditional TV still sees the majority of TV viewing overall, but this is not the case when we isolate for younger viewers, who grew up with smartphones and YouTube and spend more time on digital platforms.

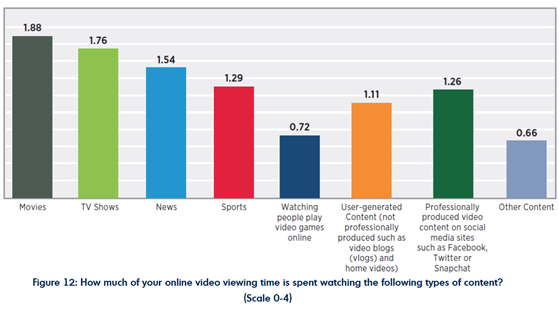

While influencer and user-generated videos are highly popular with younger viewers, the general population spends more time watching movies, TV shows and other professionally produced videos, even on social media. This is good news for investors in original programming, which may just be paying off. One out of every three people watches originals (such as those found on Netflix and Amazon), and this audience is younger and even more diverse than the general audience for online TV shows.

Source: Limelight Networks State of Online Video 2018

But where are they watching? For those 35 and under, mobile is the primary screen for watching online videos, and viewership here will continue to grow. For premium content, connected TV devices (Roku, Chromecast, etc.) are quickly becoming the favored medium. More than half of premium video ad views are on connected TVs, and premium video content views rose 31% in Q2 over last year, according to FreeWheel.

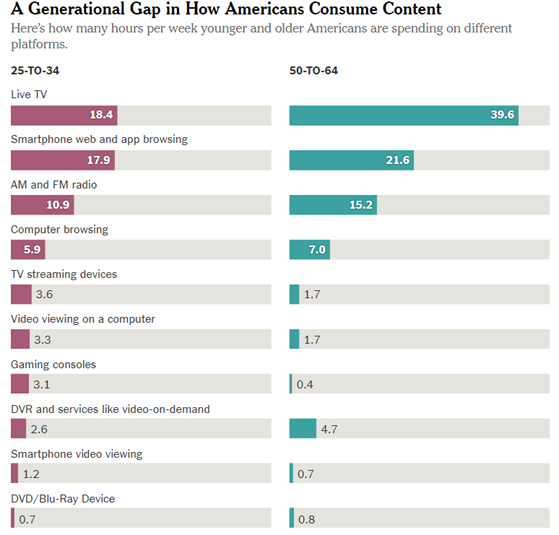

Each new generation consumes content in different ways. The chart below from The New York Times illustrates the gap in weekly hours spent watching live TV between younger and older Americans, as well as the variety of devices younger Americans view videos on. Expect this gap to widen even more as Gen Z enters the workforce in a few years.

Source: The New York Times

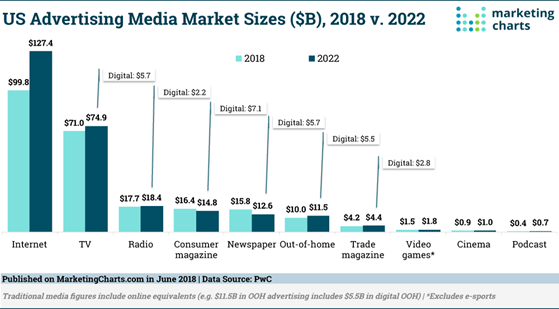

As ad dollars continue to shift to digital, competition for TV ad budgets intensifies.

Digital ad spend surpassed TV spend for the first time last year, driven by growth in mobile video consumption and social media. For video specifically, sport content was a big driver. Sixty percent of digital marketing budgets will be spent on online video.

Feeling the pressure from Google and Facebook, the TV industry continues to invest in data-enabled ad delivery capabilities. TV networks are joining forces with efforts such as the Open AP consortium (Turner, Fox, Viacom and now NBCU) to improve targeting and measurement on traditional TV. AT&T acquired AppNexus and rebranded its ad unit as Xandr. It strengthens its position in the digital ad market with a more robust ad tech stack, content from Warner Media, and its mobile and DirecTV distribution platform.

The competition for the more than $70 billion TV budget continues to intensify as both tech and media companies offer new services and expand existing ones. Roku, now with more than 22 million users, plans to expand its advertising inventory on and off Roku devices via the Roku Channel. Google lets advertisers buy inventory on its live TV offering YouTube TV, which it reports now reaches 85% of U.S. households, and will allow targeting on connected TV devices going forward. Amazon, which is now the third-largest digital ad platform after Google and Facebook, plans to launch its own ad-supported video service.

Consolidation and collaboration define the new world order.

The cable and broadcast industry is experiencing seismic changes, many of which are driven by evolving consumer behaviors and intensifying competition from big tech companies. The impact of the generational shift in viewing behavior will be deep and transformative and is already being felt, with millennials watching less traditional TV.

Skinny bundles have been the response from operators and tech companies targeting cord-cutters and cord-nevers (and the advertisers looking to reach them). The adoption of skinny bundles over the past year has helped slow the decline of pay TV (DirecTV Now subscriptions now sit at 1.8 million and Sling TV at 2.3 million). But while these services are keeping customers in the ecosystem, pay TV is still under challenge. Operators will either need to reduce cost by investing in their own content or reduce license fees (AT&T is well-positioned here with Warner Media), or increase revenues by increasing price, ad sales and/or subscribers—a challenging feat given the growing number of alternatives.

Tech companies such as Amazon and Apple, on the other hand, view content as a vehicle for customer acquisition and can balance their spend against revenues from other products and services. These companies continue to grow in the sector as they invest billions into video to compete for talent, advertisers and audience.

Facebook launched IGTV earlier this year to compete with YouTube (and everyone else). While premium content isn’t core to Google’s or Facebook’s video strategies, the two are most responsible for shifting attention and time to online and mobile. Eight of the top ten apps in 2017 were theirs. Amazon Prime continues to grow, surpassing YouTube in streaming popularity in the United States, according to Sandvine, and is available in 200 countries (YouTube still has a significant lead globally). Apple, which has invested $1 billion in original content, will be giving away that content for free to Apple users and as part of its TV app—not unlike the Amazon Channels model (an aggregation of SVOD services that allows users to pick and manage their subscriptions). Apple and Amazon are starting to look like pay TV providers as they re-bundle services.

Finally, Netflix is estimated to spend a whopping $13 billion this year (more than double its 2017 budget), and 85% of the spend is going to original content. With 56 million users in the United States and 130 million globally, Netflix is rewriting the rules of TV and forcing the rest of Hollywood to catch up.

Nothing exemplifies the seismic changes in premium video more than the recent consolidation in the industry—Disney/Fox, AT&T/Time Warner and Discover/Scripps—and their direct-to-consumer (DTC) priorities. These deals create content behemoths large enough to go head-to-head with Netflix. Comcast is also exploring DTC initiatives with NBCUniversal and is expanding its international footprint with its pending acquisition of U.K. broadcaster Sky.

Outside of these giants, collaboration across the ecosystem has been key to responding to these changes. Networks are finding homes in skinny bundles and other new services. Philo, a skinny bundle with no broadcast or sports channels, raised $40 million this summer from AMC, Discovery and Viacom. Walmart, an unlikely new entrant, is partnering with MGM to help boost its Vudu streaming service. In an attempt to slow down cord-cutting, many of the pay TV providers are offering access to streaming services such as Netflix on their platforms.

Evolving consumption behaviors and pressure from Hollywood outsiders are challenging historical roles and business models, and are continuing to define what it means to watch TV.