Published On

March 9, 2023

Author

SEC New Pay Versus Performance Disclosures – They Are Here!

Background

On August 25, 2022, the Securities and Exchange Commission (SEC) adopted final rules implementing the pay versus performance disclosure required by Section 935(a) of Dodd-Frank, effective for executive compensation disclosures for fiscal years ending on or after December 16, 2022 (PVP Disclosure Rules).

The PVP Disclosure Rules require the following:

- Tabular Disclosure

- Comparative Disclosure

- Tabular List Disclosure (Non-SRC Issuers only)

Tabular Disclosure

An Issuer is required to provide three years of disclosure in the first year of disclosure, four years in the second year of disclosure and five years thereafter. For small reporting companies (SRCs), two years are required in the first year of disclosure, then three years thereafter.

Compensation Disclosures

The Issuer must disclose, in the tabular format provided below, the compensation paid to the principal executive officer (PEO) and the average compensation paid to the other named executive officers (Non-PEO NEOs). The Tabular Disclosure provides a comparison for the PEO and Non-PEO NEOs between the total compensation paid, as reported in the Summary Compensation Table (SCT), and the Compensation Actually Paid (CAP) as determined under the PVP Disclosure Rules.

CAP is calculated using the totals reported for the PEO and each NEO in the SCT. Adjustments are made to the SCT totals to recalculate the equity compensation and pension plan accruals for each fiscal year. CAP is reported in the Tabular Disclosure for the PEO, and the average CAP is reported for the other Non-PEO NEOs. The CAP adjustments should be provided as a footnote disclosure to the Tabular Disclosure, along with any other information that provides clarity and context to the Tabular Disclosures.

Total Shareholder Return Disclosures

The Issuer must disclose its Total Shareholder Return (TSR) for each year based on the change in stock price between the beginning of the base period and the last day of each fiscal year, where the base period is the year immediately prior to the last year reported.

Peer Group Total Shareholder Return (Peer Group TSR) can be based on the Issuer’s compensation peer group or one of the comparators used in the Issuer’s performance graph. SRCs are not required to provide peer group TSR disclosures.

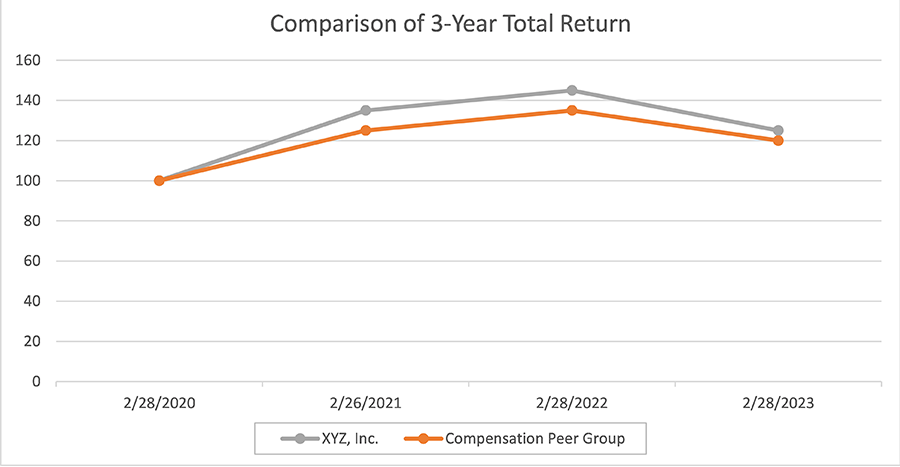

Choosing the Right Peer Group

For purposes of the Peer Group TSR in the Tabular Disclosure, the Issuer may use the compensation peer group disclosed in the CD&A or a peer group or index used in its most recent performance graph. We recommend evaluating all peer group comparators in graphical form to determine the optimal disclosure.

The final column of the Tabular Disclosure is a Company-Selected Measure. The selected financial measure should represent the Issuer’s most important financial performance measure used to link CAP to company performance. The following is an example of a peer group comparison for purposes of determining the optimal peer group.

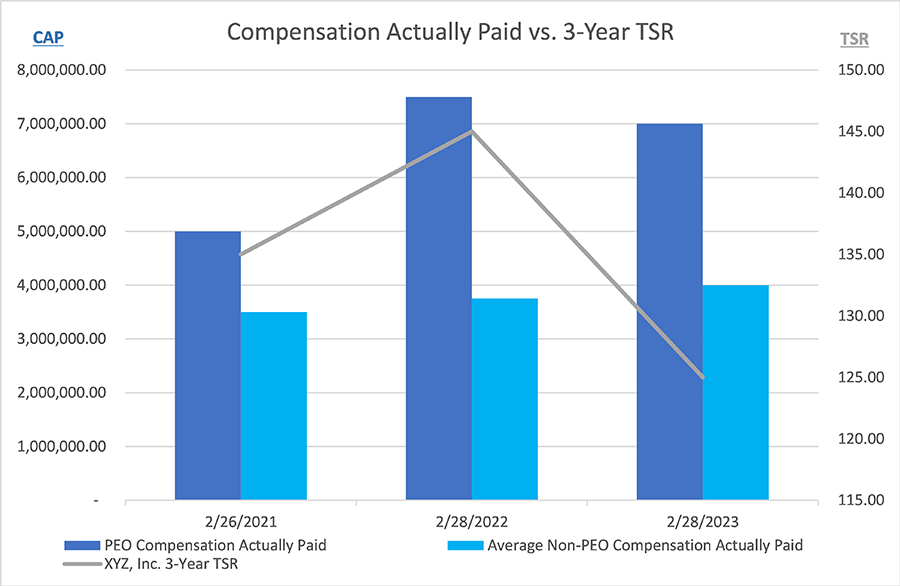

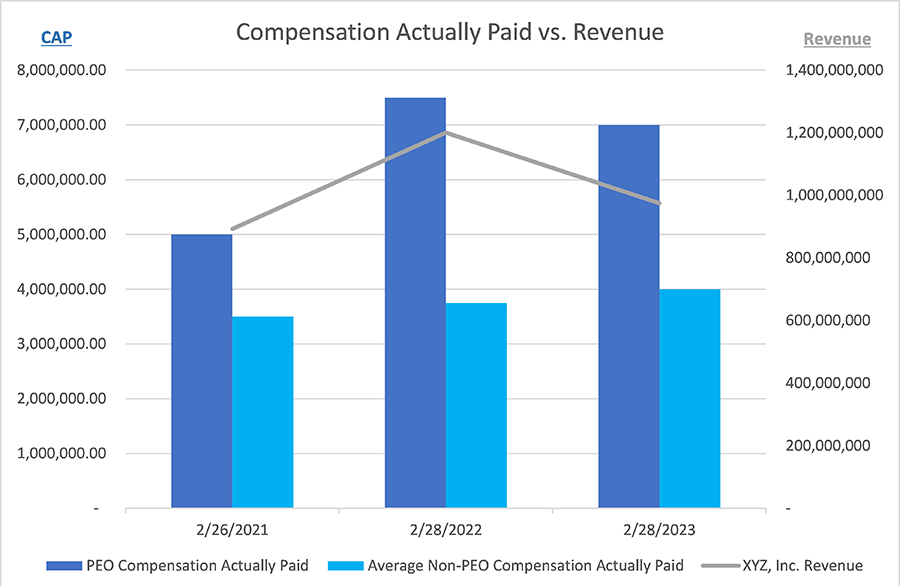

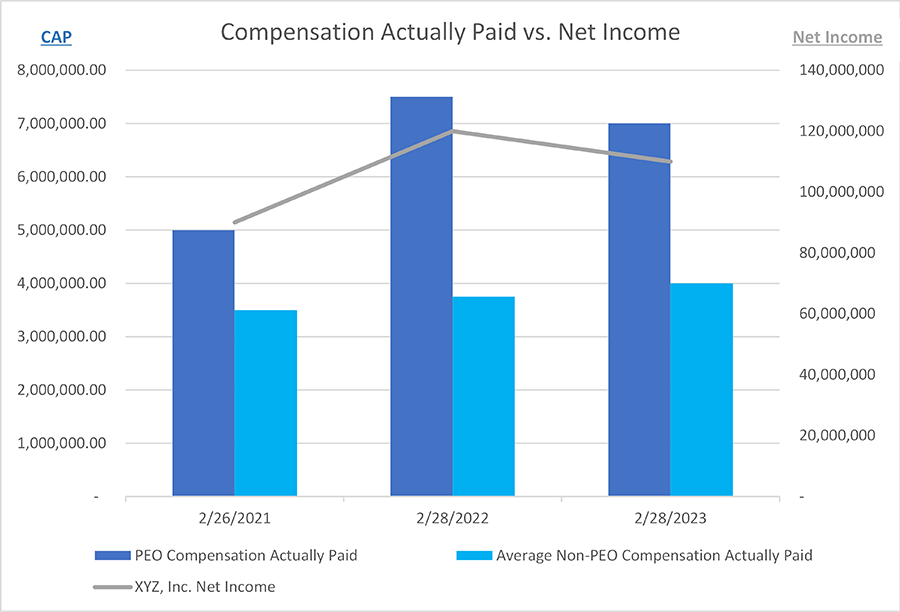

Comparative Disclosure

The Issuer is required to use the information in the Tabular Disclosure to provide a clear description of the relationship between TSR, Net Income and the Company-Selected Measure (as reported in the Tabular Disclosure) and the CAP paid to the PEO and average CAP paid to the Non-PEO NEOs. In addition, the Issuer must provide a Comparative Disclosure of the Issuer’s TSR compared with the peer group TSR (as reported in the Tabular Disclosure)—this disclosure, however, is not required for SRCs. The Comparative Disclosure may be graphical or in narrative form. The following are examples of graphical Comparative Disclosures.

Tabular List

Non-SRC Issuers are also required to provide an unranked list of three to seven of the “most important” financial performance measures (which includes the Company-Selected Measure) used to link AP to the NEOs during the last fiscal year to company performance.

The Tabular List may be presented in one of three ways: (i) one list, (ii) two separate lists, with one for the PEO and one for the remaining NEOs, or (iii) separate lists for the PEO and each of the NEOs.

The following is an example of a Tabular List Disclosure:

PEO

Absolute Stock Price

Revenue

TSR

NEOs

Revenue

Company Billings

Contribution Margin

Non-GAAP COGS

Non-GAAP EPS

Non-GAAP Operating Income

Final Comments

Given the complexity of the new pay versus performance disclosures, particularly the determination of CAP and preparation of the Comparative Disclosures, Issuers should start immediately gathering historical information and working with advisors to prepare these new proxy disclosures. Non-SRC Issuers will need to determine whether to use their compensation peer group or one of the benchmark TSR comparators reported in their most recent performance graph. The most complicated element of the PVP Disclosure Rules is calculating CAP for the PEO and Non-PEO NEOs. For Issuers that issue stock options or stock appreciation rights, the CAP calculation will entail recalculation of the fair value of these awards on the vesting dates and as of the fiscal year-end, which can be very tedious and time-consuming. Manatt’s attorneys and consultants are very adept and experienced at performing these calculations and preparing the final disclosures.