Published On

June 28, 2017

Author

The Better Care Reconciliation Act of 2017

The Better Care Reconciliation Act of 2017

By Chiquita Brooks-LaSure, Managing Director | Patricia M. Boozang, Senior Managing Director | Allison B. Orris, Counsel | Ariel Levin, Manager

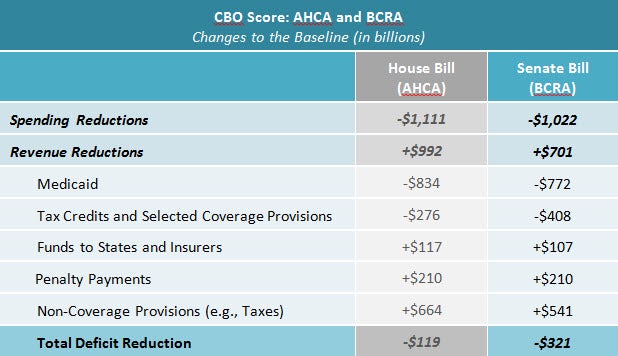

On June 22, Senate leadership released their proposed substitute for the House-passed American Health Care Act (AHCA), the Better Care Reconciliation Act of 2017 (BCRA), as a discussion draft. The BCRA was updated on June 26, and the Congressional Budget Office (CBO) released a cost and coverage score on the June 26 proposal. (See Tables 1 and 2 for more detail.)

Like the House-passed AHCA, the BCRA does not repeal the Affordable Care Act (ACA) in its entirety. It repeals the individual and employer mandates, modifies the premium tax credits, dramatically restructures Medicaid financing and, while it maintains authority for the ACA Medicaid expansion, it would eliminate enhanced federal funding over a three-year period. Together, these provisions will lead to significant reductions in Medicaid spending and coverage. For those currently covered through Marketplace plans, the BCRA reduces the value of the subsidy that individuals receive and shifts more of the cost of care to individuals. Like the AHCA, the CBO estimates that the BCRA will result in significantly less coverage in 2026 compared to current law (the ACA): 22 million more individuals will be uninsured under the BCRA as compared to coverage levels under the ACA, compared to the CBO’s estimate of 23 million more uninsured under the AHCA.

It is unclear at this time whether all of the provisions in the legislation would meet the “Byrd” rule (provisions must have a primary budget focus) and other reconciliation requirements.

Key Takeaways:

- Coverage. The CBO estimates that the number of uninsured will increase substantially from current law (the ACA). The loss in coverage is “disproportionately among the older people with lower incomes,” particularly for people between 50 and 64 with incomes under 200% of the federal poverty level. For Medicaid, the CBO estimates 15 million fewer people covered in 2026; the decline is attributable both to those currently eligible for Medicaid coverage and to those who might have been covered in the future under the ACA. The lower Medicaid coverage number for the BCRA (vs. the AHCA) appears to be the result of a lower per capita trend rate beginning in 2025. For those with Marketplace coverage, the CBO estimates 7 million fewer people covered in 2026. The CBO assumes few low-income people, despite qualifying for tax credits, would purchase coverage given the size of the deductible and cost sharing likely to result from the BCRA.

- Medicaid.

- The CBO estimates that the BCRA would reduce Medicaid spending by $772 billion over 10 years, largely as a result of the reduction and termination of enhanced expansion funding and the per capita cap. In 2026, the CBO projects that spending on the program would decline by 26% relative to current law spending projections. Although the CBO cannot quantify the impact outside of the 10-year budget window, it notes that over the long term, savings from Medicaid would continue to grow and enrollment would continue to decline, beyond the 15 million fewer people covered under Medicaid by 2026, relative to current law.

- A per capita cap would be imposed for virtually all populations, other than children who qualify for Medicaid based on disabilities, and the BCRA tightens the caps relative to the AHCA. The BCRA reduces the per capita cap growth rate for all eligibility groups in 2025, and the CBO finds that starting in 2025, the growth rate of Medicaid under current law would exceed the growth rates of the per capita caps for all groups covered by the caps. Therefore, the CBO notes that the gap between current and projected Medicaid spending under the BCRA would continue to widen because of the compounding effect of spending growth rates. As a result, the CBO estimates that spending and enrollment would continue to fall after 2026, relative to current law.

- States have the option of covering low-income parents and pregnant women (i.e., non-expansion, non-elderly, non-disabled adults) through a block grant. The CBO expects that the block grant option would be attractive mainly to the small number of states that expect to see a decline in population; therefore, the CBO expects this provision to have little effect on enrollment.

- The enhanced matching rate for the Medicaid expansion is eliminated, phasing out over three years beginning in 2021; all states can cover expansion adults at the regular match rate. The CBO does not provide a separate score for this provision but notes that some states that have already expanded coverage would drop coverage and that, relative to current law, no additional states would expand Medicaid, which would reduce enrollment and spending relative to current law.

- Medicaid Disproportionate Share Hospital (DSH) cuts will go into effect—and stay in effect—for expansion states, while non-expansion states would be exempt from all DSH cuts. The CBO estimates that this provision will increase outlays by $19 billion over 10 years.

- States’ ability to rely on provider taxes would be limited by a provision that phases down the threshold from 6% to 5% beginning in 2021. The CBO estimates that this provision will save $5 billion over 10 years.

- Affordability. The CBO estimates that, on average, premiums will be 30% lower than current law (ACA) in 2020, after increases in premiums in 2018 and 2019.1 However, the value of the coverage will be lower under the BCRA as compared to the ACA, as individuals will pay a higher portion of the cost of care. Thus, the CBO indicates that even though some individuals would pay a lower percentage of income for coverage than under current law, given the lower value of the coverage, “few low-income individuals would purchase any plan.”

- Requirement for coverage. The individual mandate is repealed retroactively, and the June 26 update to the Senate substitute provides a six-month waiting period for those who cannot demonstrate 12 months of continuous coverage. The CBO estimates that this policy will slightly increase the number of people with insurance on a net basis compared to coverage numbers without this policy.

- Market stability. The CBO estimates that under the BCRA, the individual market is stable in most parts of the country. The CBO estimates that for a few years after 2019, there would be some areas of the country with no insurers participating (because of decreased demand for coverage) or insurance only offered at very high premiums (fewer subsidized individuals resulting in less healthy people likely to enroll). The CBO estimates that states would resolve instability in their markets with (a) waivers, (b) using the funding provided under the BCRA, and/or (c) using state funding.

- State waivers for the individual market. The draft streamlines the State Innovation Waiver option (Section 1332) allowing states to waive or modify key ACA provisions, including essential health benefits and tax credits, without having to meet consumer protection guardrails previously in place. The CBO estimates that additional waivers under 1332 are likely and those waivers would (a) be used to resolve market instability in some areas, (b) probably cause market instability in other areas, and (c) lower average premiums for benchmark plans in most states with waivers. The CBO also estimates that federal deficits would increase and the number of people with health coverage would be about the same.

- Cost-sharing reductions. Cost-sharing reductions are funded in the short term, providing needed certainty to insurers and individuals, but then completely eliminated in 2020, which will significantly increase the cost-sharing that low- and middle-income individuals will pay out-of-pocket for care.

Table 1: Net Change to the Federal Deficit

Table 2: Net Changes to Coverage

Key Provisions for the House-passed AHCA and Senate-proposed Substitute BRCA

Click here for a summary of the major provisions of the legislation in a side-by-side comparison of the key House vs. Senate provisions.

Manatt Insights: New Publication with Ongoing Health Reform Updates

Manatt has launched a new publication, Manatt Insights, designed to provide timely updates on key health reform developments, as they occur at the federal and state levels. If you would like more information or to subscribe, please contact Chiquita Brooks-LaSure, Managing Director.

1Average premiums after 2020 will be lower than under current law.