Published On

November 22, 2016

Related People

The Evolving State of TV

- Video Content Consumption (Then and Now)

- What’s Next in OTT

- Is TV Achieving Digital Transformation Through M&A and Investment?

- The New TV Ecosystem

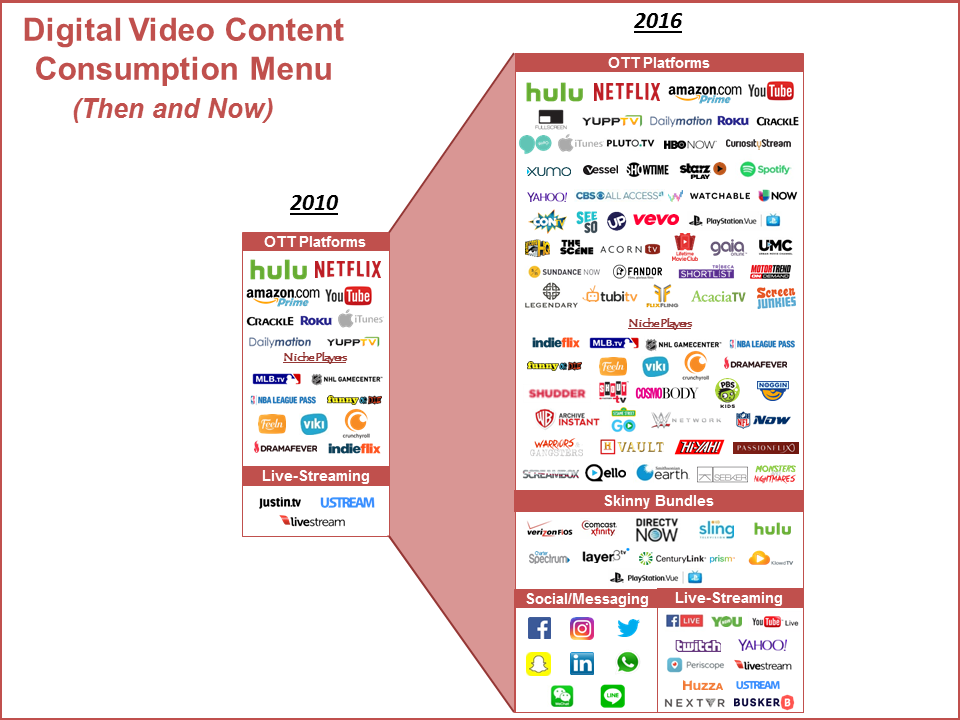

Video Content Consumption (Then and Now)

By Jordan Pritchett

It’s no secret that the digital-content-consumption landscape is evolving and at an increasingly rapid clip. One byproduct of this ongoing progression is that oftentimes consumers and organizations alike are finding themselves hard pressed to keep up with the vast array of new options that are at their disposal within the marketplace.

In order to offer some measure of clarity on the subject, we thought it would be beneficial to create the below infographic to highlight some key areas of the ecosystem that have witnessed pronounced change in recent years. While not an exhaustive representation of all your available options for each given category, the visual is helpful in underscoring some of the more important trends that are impacting the ways in which people consume their video entertainment.

- Arguably the most apparent change that has occurred during this time is the noticeable rise in “OTT Platforms” and the associated “Niche Players.” The heavyweights, to their credit, have held their ground, diversified their business models and in some instances moved toward becoming international brands. Still, competitors are on the rise, both in the form of new aggregators and niche content providers. Content is king, and it is increasingly becoming a buyer’s market.

- Because of this proliferation of content destinations, “Skinny Bundles” have stormed their way into the digital vernacular. Due in part to the response of PayTV providers seeking to retain their user base, it’s important to note that even a few “OTT Platforms” have begun to join the fray, seeking to take advantage of what has proven a compelling offering in the minds of consumers. In other news, significant consolidation has occurred under the PayTV banner with organizations moving to leverage economies of scale to curb mounting subscriber losses while also combating the growth of their more nimble counterparts.

- From a social perspective, we have witnessed a number of new entrants that are helping to reinvent what the content consumption experience entails. The most innovative and effective have endured a measure of copy catting and likely returned the favor in some form. Live-streaming serves as a good example of this. While not a wholly new idea, its popularity has exploded in recent years. The big fish are investing big capital to build out their respective platforms and seeking to capitalize on their extensive reach. Tangentially, VR adoption is still in its infancy, but look for it to play an increasingly prominent role in the worlds of both content and social engagement.

What’s Next in OTT

By Eunice Shin

For those who preach “content is king,” there’s never been a more exciting time, with the continued growth of companies in OTT services, including all the new skinny bundles and niche OTT platforms. And for audiences the good news is that you can pretty much watch whatever content you want. The bad news is the experience to find it. With so many OTT offerings, packaged and offered in so many different ways, content discovery is the next big challenge for the OTT market.

For the cord-cutters, cord-nevers and cord-forevers, one still common thread is that customers are given a plethora of choice in content and need to be given a reason to engage with that content. And with the TV market producing more shows than ever before, and with the proliferation of niche services and aggregators across services, how will customers find and engage with new content? The argument exists that content discovery will be ruled by the feed, and that the mobile-first feed is ruled by an oligopoly. Check out related market research from Activate here and industry predictions from Redef here.

There is a lot of conjecture on the future of OTT; we are still in the early days. Will customers want to manage or pay for 10 different OTT subscriptions? What happens with live sports? Will we move back to an aggregated approach after fighting the cable 300-channel model?

However, there are things from my day-to-day activities that give me a sense of what will work for me as a huge consumer of content.

- I love that I get equal amounts of interesting content as I do my friend’s kids’ soccer tournament pictures in my social feed. But when it comes to intriguing content, the trauma from click bait has garnered up issues of trust, and after being burned so many times, the experience has been scarred.

- Recommendations matter. Whether it’s the latest skincare I want to try or the next original series I’m looking to binge, I look to my friends to see what they recommend—e.g., Stranger Things, anyone? The influence my social network has on me is significant, and I can easily be swayed by someone I trust.

- I am not as patient as I used to be. The days of scrolling through the channel guide or searching through catalogs to find something to watch are over for me. I want ease, speed and quality—on every device. Well, don’t we all?

Whether it’s the social feeds, mobile devices, or the smart/connected home and TV, my bet is on the technology that offers the best customer experience in navigating through content, making recommendations based on my influencers (friends, tastemakers), and delivering an ease with as few clicks as possible. Wherever a company sits in the OTT ecosystem—content licensor, distributor, advertiser/brand—there is a keen eye looking for who can help them win in content discovery. To which I say, if content is king, then customer experience is the queen who rules the king.

Is TV Achieving Digital Transformation Through M&A and Investment?

The decline of traditional television has been predicted for years. The threat of YouTube and Netflix, cord-cutters and cord-nevers, and the overall emergence of mobile content consumption have caused hand-wringing throughout the industry for quite a while. In previous years there were trends and forecasts suggesting that the television industry was in jeopardy, but it appears that 2016 may be the year where TV finally faces that challenge head-on.

Traditional pay-TV subscriptions are down by almost a half million in Q3, which is about what happened in the same time last year. ESPN, the cash cow of pay-TV subscriptions, lost 621,000 subscribers for November alone according to Nielsen data. Even the NFL ratings are down across the board for Thursday, Sunday, and Monday Night Football; MNF is down 24% year over year. Consumers are moving away from traditional TV in ways that are now having an economic impact on the industry. However, the major networks and studios have not been sitting idly by. They have been making deals throughout the year to both consolidate power and diversify their interests in a way that keeps them relevant through the digital transformation.

AT&T’s $85 billion acquisition of Time Warner has major ramifications in the television industry. It allows AT&T and DirecTV to become more vertically integrated by owning a stack of television content creators and distributors. It also makes them more competitive with Verizon and Comcast, which have both taken a similar approach to the direction of the industry.

Until recently one of the biggest transactions in the TV world was Comcast acquiring DreamWorks Animation for $3.8 billion. This deal not only brought Comcast a feature animated film studio, it also included AwesomenessTV. Now NBCU can leverage content from a host of producers and distribution platforms to attract audiences that traditionally may not consume TV content on TV. Comcast also acquired the sports-data tech company OneTwoSee, in an effort to enhance its X1 offering for live sports content, which is still one of the biggest drivers of TV advertising revenue.

In addition to consolidation, diversification of core business has been a key driver of deals in 2016. NBCU’s push into digital publishing has continued with $200 million of additional investment into BuzzFeed (on top of the $200 million they invested last year). After their $200 million investment into Vox Media last year, NBCU is now realizing some benefits of that transaction with a new offering called Concert that allows advertisers to reach premium ad inventory across Vox’s eight digital publishers and all of NBCU’s digital properties.

Not to be left out in the cold, Discovery Communications recently invested $100 million into Group Nine Media. This move is mutually beneficial, leveraging Group Nine’s content across Discovery’s platforms, including traditional linear TV, as well as giving Discovery a stronger foothold in the digital media space.

Turner, Univision and AMC Networks have also put their money into the digital space in 2016, with Turner leading a $15 million round in Mashable and leading a $45 million round in Refinery29. Univision acquired the remnants of Gawker Media for $135 million, giving them an asset to reach millennials and other non-TV audiences who look to digital for content. AMC Networks recently acquired a minority stake in the online comedy production and distribution company Funny or Die (FoD). This deal allows FoD and AMC’s independent-focused channel IFC to cross collaborate and bring successful digital-first projects to traditional television.

Time Warner further committed to the digital distribution model with a 10% investment into Hulu for a reported $538 million. With their content already moving towards a digital model via HBO NOW and WB’s acquisition of DramaFever and Machinima, the acquisition fits their continued strategy of meeting their audience where they are consuming content. With the upcoming AT&T integration, Time Warner could find a home with a like-minded partner, as the upcoming DirecTV Now OTT plan will be yet another place for Time Warner content to live.

Disney has made a sizable bet on the future of digital distribution with a $1 billion investment for 33% of MLB’s BAMTech. In addition to the tech, Disney invested in digital content creator and distributor Vice Media at the end of 2015, hoping to reach a millennial audience that is loyal to the Vice brand.

One of the interesting new areas that traditional TV companies are investing in is virtual reality (VR). Disney led the $65 million round in Jaunt, while live-streaming VR company NextVR has received over $115 million in funding from Time Warner and Comcast, among others.

With all of the activity in 2016, it’s clear that traditional TV operators realize that they need to be directly involved in the new digital distribution and content opportunities. Since the digital ecosystem develops and moves so quickly, it makes sense that the TV industry is using their significant capital to buy a seat on the train. As 2016 winds down, it appears that 2017 will allow consumers more options than ever before to consume content in a way that fits their preferences.

The New TV Ecosystem

By Mary Ermitanio

On October 14, 2016, two high school football teams in Arkansas, Pulaski Academy and Sylvan Hills, went head-to-head in a game that was broadcast live on Facebook by Bleacher Report. While the game itself had little significance to most of us outside of Arkansas, the event exemplifies a greater shift impacting the media, entertainment and advertising industries—the evaporating boundaries that define what we know as “traditional” TV. Cord cutting and over-the-top (OTT) streaming have been the buzzwords of the last few years, used to describe the evolution of TV consumption habits. But this example speaks to other facets of the industry’s transformation: the emergence of new content producers, content distributors and new iterations of live programming.

Content Creation. New entrants redefining TV content include former print- and text-based publishers, consumer brands, digital-first studios and tech companies, each having disparate motivations.

Publishers. Publishers seek to offset loss of revenues in their traditional businesses, which relied primarily on display ads or sponsored content. Many have gone “all-in” in video, including expansions to emerging forms of video such as live streaming, 360-degree videos and virtual reality. Video accounted for 15% of BuzzFeed’s revenue at the end of 2014; in two years this number is expected to rise to 75%. The New York Times, which aims to make video as common as text in its reporting, has announced The Daily 360, a platform delivering one 360-degree video a day.

Digital-First Studios. Over the last few years, dozens of studios have been launched by Hollywood and “digital-first” talent with industry collaborations to express their creativity or serve niche audiences on digital platforms. These include Ron Howard and Discovery’s New Form Digital and Lionsgate and Kevin Hart’s Laugh Out Loud comedy video service.

Consumer Brands. While it is more common for brands to pay for advertising around TV content, many have forayed into original programming themselves. Starbucks, for example, debuted its first original series, Upstanders, which tells stories around citizens creating positive changes in society and is available on its app and online properties. Through content, these companies seek to connect more intimately with their target audiences and create a stronger impression of their brand.

Tech. Technology companies, such as Amazon, Apple and Google (via YouTube), are also creating original content to attract new customers onto their platforms and to serve as a value-add for existing customers. Needless to say, former pure-play digital distributors Netflix and Hulu have contributed early on and in a large way to TV’s transformation. Central to TV’s transformation are these and other technology companies, which have played the role of both nontraditional content producers and content distributors.

Content Distribution. Further complicating the definition of TV, nontraditional content distributors are paying the various types of creators—online publishers, social influencers, digital-first studios, in addition to traditional media companies—for access to their content, a model analogous to the way TV networks have worked with cable and satellite operators. Facebook has paid many publishers, including Huffington Post and Hearst, to produce live videos for Facebook Live. Twitter acquired the exclusive rights to stream the NFL’s Thursday Night Football this year and brought in 2.3M viewers in its first week. Snapchat is replacing the ad revenue sharing model it uses with media companies with the old TV network license fee model.

Live Video. Live sports and news have been considered immune to the evolving nature of TV. However, the shift of publishers (many news- and sports-focused) to digital, combined with the push on live-streaming features by major platforms, pose both challenges and opportunities to broadcasters in the space. YouTube saw an 80% increase in live viewership over the last year. Facebook, Snapchat and Twitter are promoting their live-streaming features heavily in terms of content partnerships, as well as in their user experience. Features such as Facebook’s Live Button and Push Notifications and the coverage of live events across all three platforms have increased the role of live video in social networks, where consumers spend at least a third of their time on mobile, according to Flurry Analytics.

Bleacher Report’s Facebook broadcast of the high school football game had a familiar setup, with multiple camera angles, commentators and the first down line; however, it was augmented with real-time reactions and comments. Coverage of the election on Facebook, Twitter and other platforms was interactive and social.

To a new generation of viewers, TV will be much broader. It will encompass live and on-demand content from both major networks and digital-first studios, consumer brands and online publishers, delivered across streaming services, social networks and satellite and cable providers.