Published On

March 30, 2020

Related People

Congressional Action—Lending Programs and Relief Provisions Under the CARES Act

Background

On March 27, 2020, President Donald Trump signed into law the CARES Act, an approximately $2 trillion stimulus package to mitigate the adverse economic effects of the COVID-19 pandemic. President Trump signed the CARES Act hours after the House of Representatives passed it and two days after the Senate passed it. The CARES Act (or Coronavirus Aid, Relief, and Economic Security Act) is a multifaceted relief effort directing funds to both individuals and businesses as well as addressing the supply shortages and logistical obstacles facing healthcare providers.

The CARES Act amends certain provisions of the existing Small Business Act, the policies of which are carried out by the Small Business Administration (SBA). Generally, the SBA does not lend money directly to small business owners, but instead sets guidelines for loans made by its partnering lenders, community development organizations and micro-lending institutions. The SBA guarantees loans issued pursuant to Section 7 of the Small Business Act.

The adoption of the CARES Act is in addition to other laws that have been enacted (links to Manatt’s coverage are provided below):

- COVID-19 Update: Employee Retention Tax Credit for Employers Subject to Closure Due to COVID-19

- The Coronavirus Preparedness and Response Supplemental Appropriations Act, 2020, which was signed into law on March 6, 2020, providing $8.3 billion in emergency funding for federal agencies to respond to the COVID-19 outbreak

- The Families First Coronavirus Response Act, which was signed into law on March 18, 2020, providing paid sick leave, tax credits and free COVID-19 testing; expanding food assistance and unemployment benefits; and increasing Medicaid funding

Manatt is closely watching the fast-moving legal developments related to the COVID-19 pandemic and is working hard to collaboratively share resources and information. For a collection of our insights and webinars, check out Manatt’s Hot Topics/COVID-19 web page.

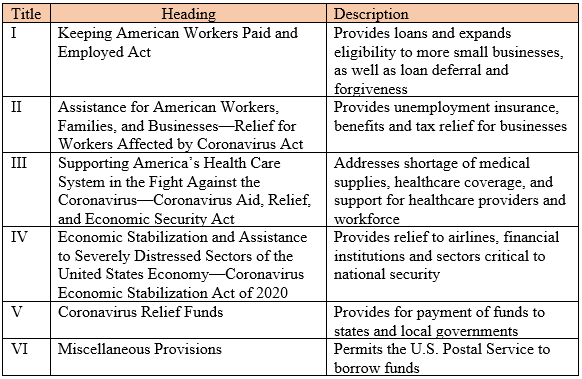

As an overview, the CARES Act consists of the following divisions and titles:

Division A—Keeping Workers Paid and Employed, Health Care System Enhancements, and Economic Stabilization

Division B—Emergency Appropriations for Coronavirus Health Response and Agency Operations

This article primarily focuses on provisions that are intended to benefit businesses included in Title I—the SBA Business Loans Program, deferral and forgiveness—and Title IV regarding loans from the Treasury’s Exchange Stabilization Fund.

TITLE I—KEEPING AMERICAN WORKERS PAID AND EMPLOYED ACT

Small Business Administration—Business Loans Program, CARES Act

The CARES Act amends Section 7(a) of the existing Small Business Act to allow the SBA to provide, for the period from February 15, 2020, to June 30, 2020 (the covered period), 100% federally guaranteed loans to eligible businesses. The Small Business Act was initially applicable only to a “small business concern,” which is generally defined as a business that is independently owned and operated and not dominant in its field of operation, subject to additional criteria which may be imposed by the SBA. The CARES Act provides $349 billion for the SBA Business Loans Program. The SBA is required to issue regulations to carry out the provisions of Title I within 15 days of enactment.

Eligible Businesses; Certification

The CARES Act expands eligibility under the Small Business Act to include, during the covered period:

- Any business (including nonprofit organizations) with not more than 500 employees, which includes individuals employed on a full-time, part-time or other basis

- If applicable, the number of employees established by the SBA as the standard for the industry in which the business operates

- Any business that employs not more than 500 employees per physical location with a North American Industry Classification System (NAICS) code beginning with 72 (accommodations and food services)

- Any sole proprietorship, independent contractor or eligible self-employed individual (as defined in Section 7002(b) of the Families First Coronavirus Response Act), each of which must provide certain documentation to establish eligibility

During the covered period, SBA regulations applicable to entity affiliations are waived for (1) any business with not more than 500 employees that has a NAICS 72 code, (2) any franchise that is assigned a franchise identifier code by the SBA, and (3) any business that receives financial assistance from a Small Business Investment Company (licensed under Section 301 of the Small Business Investment Act of 1958).

For purposes of making loans, a lender must consider whether the business was in operation on February 15, 2020, and whether it paid employee salaries and payroll taxes or paid independent contractors.

In order to receive a loan, an eligible business must certify that the following are true:

- The loan is necessary to support ongoing operations as a result of the uncertainty of current economic conditions.

- Funds will be used to retain workers and maintain payroll or to make mortgage payments, lease payments and utility payments.

- It does not have an application pending for a loan under the program for the same purpose.

- During the period from February 15, 2020, to December 31, 2020, it has not received amounts under the program for the same purpose.

In a “Sense of Congress” provision, the CARES Act requires the SBA to issue guidance to lenders and agents to ensure that the following businesses are prioritized:

- Businesses in underserved and rural markets, including veterans

- Women-owned businesses

- Businesses in operation for less than two years

- Businesses owned and controlled by socially and economically disadvantaged individuals

Maximum Amount; Loan Terms

The maximum loan amount is the lesser of:

- $10 million

or - 2.5 times either:

a) The average total monthly payments for payroll costs (see further below for list of payroll costs) incurred during the one-year period before the date on which the loan is made,1 or

b) If requested by an otherwise eligible business that was not in business between February 15, 2019, and June 30, 2019, the average total monthly payments by the applicant for payroll costs incurred between January 1, 2020, and February 29, 2020

plus the outstanding amount of an SBA disaster loan that was made between January 31, 2020, and the date that such loan is refinanced with a loan under the CARES Act.

Loans given under the CARES Act will have the same terms, conditions and processes as loans provided under the existing Small Business Act. However, loans under the CARES Act will include the following features:

- All loans bear an interest rate of not more than 4%.

- All loan fees will be waived.

- Personal guarantee and collateral requirements will be waived.

- There will be no prepayment penalties.

In addition, unlike loans under the current SBA loan program, the condition that the business is unable to obtain credit elsewhere is not required. Plus, there is no recourse against any individual shareholder, member or partner for nonpayment of any loan, except to the extent that such shareholder, member or partner uses the loan proceeds for a purpose not authorized.

Permissible Uses

Loans issued under the Small Business Act may currently be used for a variety of general business purposes, including working capital, machinery and equipment, furniture and fixtures, purchasing or renovating land and buildings, leasehold improvements and debt refinancing.

Loans under the CARES Act can also be used to help cover the following:

- Payroll costs (see below for specifics)

- Healthcare benefits for paid sick, medical or family leave, and insurance premiums

- Employee salaries, commission or similar compensation

- Rent

- Mortgage interest payments (excluding prepayments or payments of principal)

- Utilities

- Interest on any other debt obligations that were incurred before the covered period

Payroll costs are defined as follows:

- Include salary, wage, commission or similar compensation; cash tip or equivalent; vacation, parental, family, medical or sick leave; allowance for dismissal or separation; group healthcare benefits, including insurance premiums and retirement benefit; state or local taxes; and sole proprietor or independent contractor compensation of up to $100,000 in one year, as prorated for the covered period.

- Exclude individual employee annual salary of more than $100,000, as prorated for the covered period; taxes under chapters 21, 22 or 24 of the Internal Revenue Code of 1986 during the covered period; compensation of an employee whose principal place of residence is outside of the U.S.; and qualified sick leave and family or medical leave wages for which a payroll tax credit is allowed under the Families First Coronavirus Response Act.

Loan Deferrals

Business that were in operation on February 15, 2020, and that have a pending or approved loan application under this program are presumed to be adversely impacted by COVID-19. This means that these businesses qualify for complete payment deferral (principal, interest and fees) on loans for a period of at least six months but not more than one year. Payment deferral is required to be provided during the covered period. Plus, if secondary market investors decline to approve a deferral requested by a lender, then the SBA must purchase the loan. The SBA is required to provide guidance to lenders on the deferment process within 30 days from enactment of the CARES Act.

Loan Forgiveness

A lender may forgive up to the principal amount of a loan, which amount, however, may be reduced based on any reduction in the number of employees or the amount of their compensation, each as described below. The amount that may be forgiven consists of the following costs incurred and payments made during the eight-week period beginning on the origination date of the loan:

- Payroll costs (see above for specifics)

- Additional wages paid to tipped employees (as described in the Fair Labor Standards Act of 1938) may also be forgiven

- Interest payments (excluding prepayments or payments of principal) on mortgage debt on real or personal property2

- Rent payments on a lease2

- Utility payments—electricity, gas, water, transportation, telephone or internet access service2

Any remaining balance of a loan after forgiveness will continue to be guaranteed by the SBA, and the loan will have a maximum term of 10 years from the date on which the business applies for loan forgiveness. The SBA must pay to the lender the amount that was forgiven, plus any interest, within 90 days after the date on which the amount was forgiven.

Reduction for Salary and Wages

The amount of loan forgiveness will be reduced by the amount of any reduction in wages and salary that:

- was paid during the eight-week period to any employee who did not have an annualized rate of pay of more than $100,000 during any single pay period during 2019,

and

- is in excess of 25% of the total salary or wages of the employee during the most recent full quarter during which the employee was employed before the loan origination date.

Reduction in Number of Employees

In the case of a reduction in employees, the reduction in loan forgiveness is calculated by multiplying the loan amount using the following formula:

The average number of full-time equivalent employees is determined by calculating the average number of full-time equivalent employees for each pay period falling within a month.

Exception for Rehiring Employees; Making Up Wages

The CARES Act provides an exception to the forgiveness reduction for businesses that rehire employees or make up wage reductions by June 30, 2020.

If:

- During the period between February 15, 2020, and 30 days after enactment of the CARES Act (likely April 28, 2020) there is a reduction, as compared to February 15, 2020, in the number of full-time equivalent employees and/or in the salary or wages of one or more employees.

- Not later than June 30, 2020, the employer has eliminated the reduction in the number of full-time equivalent employees and/or the reduction in the salary or wages of such employee.

Then:

The amount of loan forgiveness will be determined without regard to a reduction in the number of full-time equivalent employees or a reduction in the salary of one or more employees, as applicable, during the period between February 15, 2020, and 30 days after enactment of the CARES Act (likely April 28, 2020).

A business with tipped employees (described in the Fair Labor Standards Act) may receive forgiveness for additional wages paid to those employees. Additionally, the SBA and Secretary of the Treasury may prescribe regulations granting de minimis exemptions from these requirements. However, loans issued under the expanded disaster loan program (Title IV—as described below) may not be forgiven.

Any qualified sick leave and family or medical leave wages that are used in the calculation of the loan forgiveness amount are not eligible for the tax credit under the Families First Coronavirus Response Act.

Application

To obtain loan forgiveness, a business must submit the following:

- Documentation verifying the number of full-time equivalent employees on payroll and pay rates for each of the periods, including—

- Payroll tax filings reported to the IRS

- State income, payroll and unemployment insurance filings

- Documentation, including canceled checks, payment receipts, transcripts of accounts or other documents, verifying payments on covered mortgage obligations, payments on covered lease obligations and covered utility payments

- Certification that the documentation is true and correct, and that the amount of loan forgiveness requested was used to retain employees, make interest payments on a covered mortgage obligation, make payments on a covered rent obligation or make covered utility payments

- Any other documentation determined to be necessary

The lender is required to issue a decision on the application for loan forgiveness within 60 days.

The SBA is required to issue regulations on the forgiveness provisions within 30 days from enactment of the CARES Act.

Taxes

Any amount which would be included in gross income by reason of the loan forgiveness will be excluded from gross income.

Emergency Economic Injury Disaster Loans (EIDL)—Disaster Loan Assistance

The CARES Act also expands the SBA disaster loan program (Section 7(b)(2) of the Small Business Act), which provides loans of up to $2 million. The SBA has updated its application process for disaster loans, which can be accessed on online at https://covid19relief.sba.gov.

During the period from January 31, 2020, to December 31, 2020 (the disaster covered period), in addition to current eligible entities, the following additional eligible entities that were in operation before February 1, 2020, may receive disaster loans:

- A business with fewer than 500 employees

- A cooperative with fewer than 500 employees

- An ESOP (as defined in Section 3 of the Small Business Act) with fewer than 500 employees

- A tribal small business concern (as described in Section 31 of the Small Business Act) with fewer than 500 employees

- Any individual who operates under a sole proprietorship, with or without employees, or as an independent contractor

A business may be approved for a disaster loan during the disaster covered period based solely on its credit score, and it may not be required to submit a tax return for approval. Alternative appropriate methods may be used to determine a business’s ability to repay.

The following will be waived for a disaster loan made in response to COVID-19 during the disaster covered period:

- Any rules related to the personal guarantee on advances and loans of not more than $200,000

- The requirement to be in business for the one-year period before the disaster, except that no waiver may be made for a business that was not in operation on January 31, 2020

- The requirement that an applicant be unable to obtain credit elsewhere

These loans will have an interest rate of 3.75% and a term of up to 30 years. Repayment of the loan will start 12 months from the disbursement date of the loan. A personal guarantee will be required for loans of more than $200,000, and for loans of more than $25,000, collateral will be required and a $100 processing fee will be added to the amount of the loan.

Emergency Advances

A business may request an advance of up to $10,000 within three days after the SBA receives the business’s application. An emergency advance is not required to be repaid; however, if the business is approved for a loan under Section 7(a) of the Small Business Act (described above), any payroll forgiveness amounts will be reduced by the amount of the emergency advance. An emergency advance may be used to address any allowable purpose for a loan made under Section 7(b)(2) of the Small Business Act, including the following:

- Paying sick leave to employees who are unable to work due to the direct effects of the COVID–19 pandemic

- Maintaining payroll to retain employees during business disruptions or substantial slowdowns

- Meeting increased costs to obtain materials that are unavailable from original sources due to interrupted supply chains

- Making rent or mortgage payments

- Repaying obligations that cannot be met due to revenue losses

The emergency grant program will end on December 31, 2020.

Note: the EIDL application link at the SBA can be accessed at https://covid19relief.sba.gov/

Other Lenders

In addition to SBA-certified lenders already authorized to make federally guaranteed loans by the Small Business Administration, the CARES Act authorizes the Administrator of the Small Business Administration to extend authority to make federally guaranteed loans to additional lenders under the SBA.

TITLE IV—ECONOMIC STABILIZATION AND ASSISTANCE TO SEVERELY DISTRESSED SECTORS OF THE UNITED STATES ECONOMY

Coronavirus Economic Stabilization Act of 2020

Emergency Loans and Loan Guarantees to Distressed Companies

In order to provide liquidity to eligible businesses related to losses incurred as a direct result of the COVID-19 pandemic, the CARES Act has allocated $500 billion to the Treasury’s Exchange Stabilization Fund to provide loans, loan guarantees, and other investments in support of eligible businesses, states and municipalities. An “eligible business” is a U.S. business that has not otherwise received adequate economic relief in the form of loans or loan guarantees provided under the CARES Act.

The funds will be allocated as follows:

- $25 billion to air carriers and $4 billion to cargo air carriers, in the form of loans and loan guarantees

- $17 billion for businesses critical to maintaining national security, in the form of loans and loan guarantees

- $454 billion to be deployed flexibly in support of programs and facilities established by the Federal Reserve to provide liquidity to the financial system, in the form of loans, loan guarantees and other investments

Loans issued pursuant to Title IV may not be forgiven. Under the CARES Act, the Secretary of the Treasury is required to publish guidelines with respect to application procedures and eligibility requirement with respect to these funds within 10 days following enactment of the CARES Act.

Requirements

The Secretary of the Treasury may make loans or loan guarantees to eligible businesses if the Secretary determines that, in its discretion:

- Credit is not reasonably available at the time of the transaction.

- The intended obligation is prudently incurred.

- The loan or loan guarantee is sufficiently secured or is made at a rate that

- reflects the risk of the loan or loan guarantee; and

- is, to the extent practicable, not less than an interest rate based on market conditions for comparable obligations prevalent prior to the outbreak of the COVID-19 pandemic.

- The duration is as short as practicable but not longer than five years.

- Until the date 12 months after the date the loan or loan guarantee is no longer outstanding,

- neither the business nor any of its affiliates may purchase an equity security that is listed on the same national securities exchange of the business or any parent, except to the extent required under a contractual obligation in effect as of the date of enactment of the CARES Act (March 27, 2020); and

- the eligible business may not pay dividends or make other capital distributions with respect to its common stock.

- Until September 30, 2020, the business has maintained its employment levels as of March 24, 2020, to the extent practicable, and in any case it has not reduced its employment levels by more than 10% from the levels on such date.

- The business has provided a certification that it was created or is organized in the U.S. or under the laws of the U.S. and has significant operations in and a majority of its employees based in the U.S.

- The business has incurred or is expected to incur covered losses such that the continued operations of the business are jeopardized, as determined by the Secretary.

Warrants/Senior Debt

If a company’s securities are traded on a national securities exchange, then the Treasury Secretary will provide a loan only if the company issues a warrant or other equity interest of the business to the Secretary. The Securities and Exchange Commission provides a list of National Securities Exchanges. If the company is not traded on a national securities exchange, then the company must issue either a warrant/equity interest or a senior debt instrument. If the Secretary determines that the company cannot feasibly issue warrants or other equity interests, then the Secretary may accept a senior debt instrument. The Secretary may not vote shares of common stock received as a result of the warrant or other equity interest.

Federal Reserve Programs or Facilities

The CARES Act permits the Secretary to make loans, loan guarantees, and other investments as part of a program or facility that provides direct loans (not part of a syndicated loan, a loan originated by a financial institution in the ordinary course of business, or a securities or capital markets transaction) to eligible businesses.

Main Street Lending Program

The CARES Act requires the Secretary to endeavor to seek the implementation of a program or facility that provides financing to banks and other lenders that make direct loans to eligible businesses with between 500 and 10,000 employees. The annualized interest rate on the loans must not be higher than 2% per annum. For the first six months of the loan, no principal or interest will be due or payable. Companies must provide certain certifications, including that the business intends to restore not less than 90% of its existing workforce as of February 1, 2020, and that it will restore all compensation and benefits to its workers no later than four months after the termination date of the public health emergency declared on January 31, 2020, in response to COVID-19.

Limitation on Certain Employee Compensation

The Secretary may only provide a loan or loan guarantee as long as, during the period between entering into the loan agreement and one year after the loan or loan guarantee is no longer outstanding (the loan period), both of the following apply:

- No officer or employee whose total compensation3 exceeded $425,000 in calendar year 2019 (other than an employee whose compensation is determined through an existing collective bargaining agreement entered into prior to March 1, 2020) will receive (a) total compensation that exceeds, during any 12 consecutive months of the loan period, the total compensation received in 2019; or (b) severance pay or other benefits upon termination of employment which exceeds twice the maximum total compensation received in 2019.

- No officer or employee whose total compensation exceeded $3 million in 2019 may receive, during any 12 consecutive months of the loan period, total compensation in excess of the sum of (a) $3 million and (b) 50% of the excess over $3 million.

Protection of Collective Bargaining Agreement

The federal government may not condition the issuance of a loan or loan guarantee on a requirement for the business to enter into negotiations with the certified bargaining representative of the company’s business regarding pay or other terms and conditions of employment. This requirement remains in effect on the date of the loan or loan guarantee and ends one year after the loan or loan guarantee is no longer outstanding.

How Manatt’s SBA/CARES Act Response Group Can Help: Comprised of experienced attorneys representing a cross section of practice disciplines, the Manatt SBA/CARES Act Response Group provides borrowers and lenders with practical advice regarding the provisions of the CARES Act and assists these clients to navigate and obtain relief under the Act.

For More Information: Please contact any of the following professionals:

- Katherine J. Blair, Partner, Capital Markets, at kblair@manatt.com or 310.312.4252.

- Neil S. Faden, Partner, Corporate and Finance, at nfaden@manatt.com or 212.830.7181.

- David W. Herbst, Partner, Tax, Employee Benefits and Executive Compensation, at dherbst@manatt.com or 650.812.1320.

- Brian S. Korn, Partner, Manatt Financial Services, at bkorn@manatt.com or 212.790.4510.

- Craig D. Miller, Partner, Manatt Financial Services, at cmiller@manatt.com or 415.291.7415.

- Scott M. Pearson, Partner, Manatt Financial Services, at spearson@manatt.com or 310.312.4283.

- Thomas J. Poletti, Partner, Capital Markets, at tpoletti@manatt.com or 714.371.2501.

- William T. Quicksilver, Partner, Corporate and Finance, at wquicksilver@manatt.com or 310.312.4210.

- Charles E. Washburn, Jr., Partner, Manatt Financial Services, at cwashburn@manatt.com or 310.312.4372.

- Jonathan H. Lemberg, Counsel, Venture Capital / Emerging Companies, at jlemberg@manatt.com or 415.291.7402.

- Benjamin T. Brickner, Associate, Manatt Financial Services, at bbrickner@manatt.com or 212.790.4612.

- Emily P. Gelman, Associate, Corporate and Finance, at egelman@manatt.com or 310.312.4322.

- June Kim, Associate, Manatt Financial Services, at jukim@manatt.com or 212.790.4511.

- Veronica Lah, Associate, Corporate and Finance, at vlah@manatt.com or 310.312.4130.

1 In the case of a seasonal employer, as determined by the SBA, the average total monthly payments for payroll is for the 12-week period beginning February 15, 2019, or (at the election of the eligible recipient) March 1, 2019.

2 Mortgage debt, lease, and utilities services must have been incurred, in existence or begun before February 15, 2020.

3 “Total compensation” includes salary, bonuses, awards of stock, and other financial benefits provided by an eligible business to an officer or employee of the eligible business.