Published On

May 14, 2026

Authors

From Policy to Practice: Health Plan Strategies for H.R. 1 Implementation

Introduction

Significant federal changes to Medicaid and Affordable Care Act (ACA) Marketplace coverage—including H.R. 1 (the “One Big Beautiful Bill Act”) and the expiration of enhanced ACA premium tax credits (ePTCs)—will drive coverage losses, shift risk pools and raise administrative burden for health plans across the country. These changes will be especially material for provider-sponsored health plans and plans with high Medicaid/Marketplace enrollment. Plans will need to adapt by building policy-informed, data-driven, operationally agile capabilities focused on retention, product alignment and financial resilience.

By the Numbers: Impact of Federal Policy Changes

|

Key Changes and Timeline

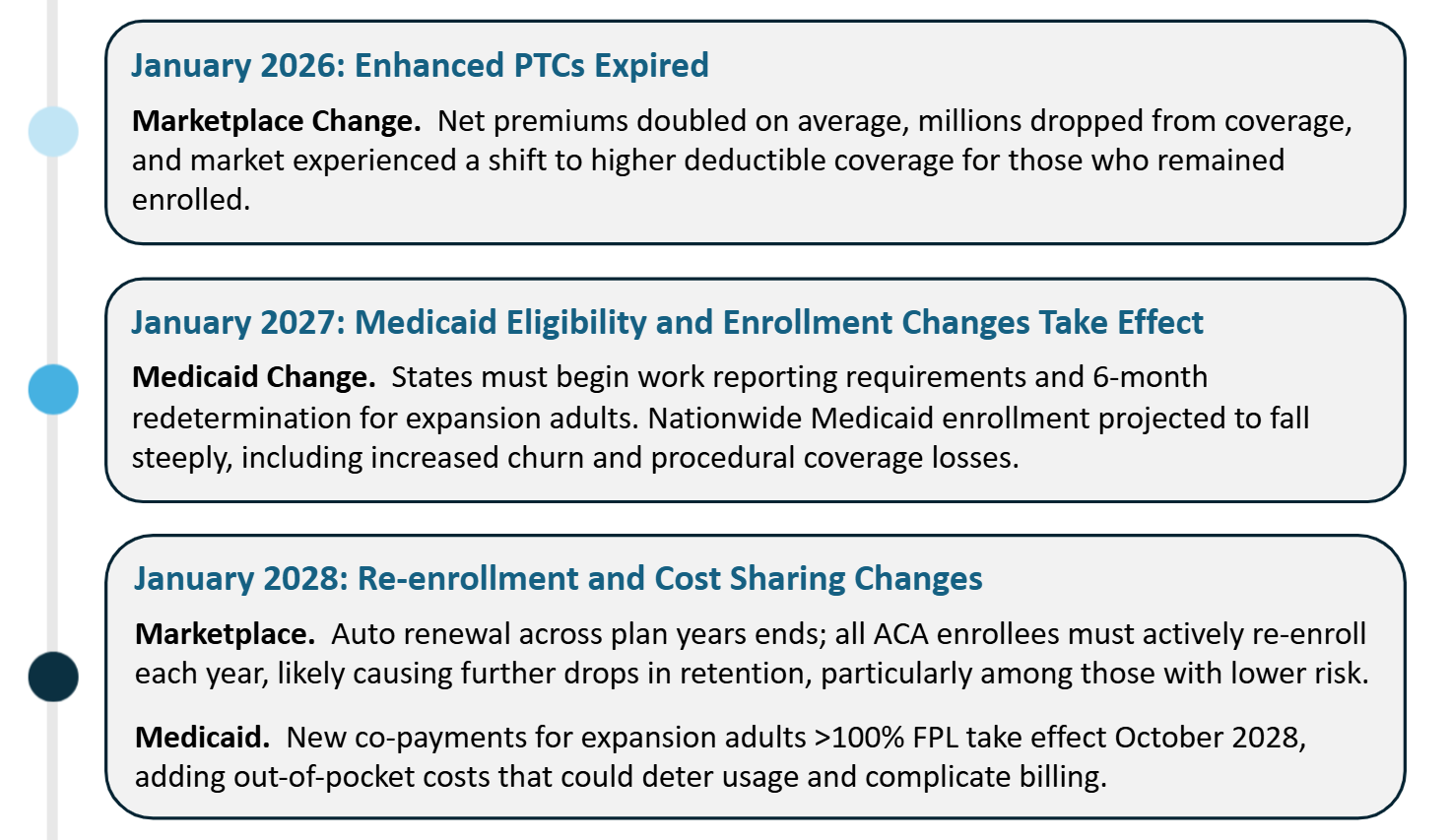

Federal changes impacting Medicaid and Marketplace plans will roll out through 2028 and will reshape both programs.

Marketplace: ePTCs ended January 1, 2026, reducing subsidies to pre-2021 levels. and H.R. 1 add additional friction, such as more burdensome verification requirements and end automatic Marketplace re-enrollment, requiring new member action each year.

Medicaid: Work reporting requirements and six-month redeterminations for expansion adults begin by January 1, 2027. H.R. 1 also shortens retroactive coverage and adds new cost-sharing for expansion enrollees starting October 2028.

Timeline of Key Changes

Major Implications for Health Plans

Coverage Losses and Risk Pool Deterioration: Experts project a significant rise in uninsurance. The Congressional Budget Office (CBO) estimates ~14 million people may lose coverage over the next decade due to H.R. 1’s Medicaid and ACA provisions and the expiration of ePTC. Manatt estimates that work requirements alone will result in ~6 million people dropping from Medicaid coverage over the next decade.

What’s more, healthier, lower-cost members are most likely to leave coverage, worsening risk mix in both programs and pressuring premiums in the Marketplace. Using data on the percentage of enrollees with January 2026 paid premiums and applying assumptions regarding average enrollment duration in 2026, a recently released report by Wakely estimates that average enrollment in the individual market could shrink 17% to 26% in 2026, with an average increase in morbidity of 2.9% to 6.5%. Disenrolled members may be hard to recapture in the Marketplace with reduced availability of zero-dollar silver CSR plans, likely driving down successful Medicaid-Marketplace transition rates to pre-ePTC conversion rates.

Medicaid plans face a parallel but distinct dynamic. As H.R. 1's eligibility and enrollment restrictions push members out of the program, those who re-enroll are more likely to need care, steadily skewing Medicaid risk pools toward higher-cost members. If states fail to adequately reflect rising acuity in their Medicaid managed care rate-setting, plans will be forced to absorb the loss, making actuarially sound rate development a critical pressure point to watch as H.R. 1 implementation unfolds.

Costlier Care Management Care management will become harder and more expensive. Increased coverage churn and a sicker remaining member base will disrupt continuity of care, make member engagement more challenging and reduce the ROI of care management programs, forcing plans to do more intensive work for fewer—and higher‑risk—members. |

Operational and Compliance Burdens: Plans should expect heavy administrative lifts related to implementation of evolving federal and state policy. In Medicaid, plans will need to support state implementation of work reporting requirements and semi-annual eligibility checks (among other eligibility and enrollment changes), take steps to mitigate churn (and its downstream impacts) resulting from increased procedural disenrollments and re-enrollments and build for new cost-sharing rules starting in 2028. In the Marketplace, the end of automatic re-enrollment will require intensive annual outreach, and shorter enrollment windows and stricter upfront verification will require greater coordination with brokers and assisters and changes to compensation arrangements. These changes drive new IT builds, member campaigns and compliance protocols, often with less premium revenue.

Double Exposure for Provider-Sponsored Plans For provider-sponsored health plans (PSHPs), coverage losses hit two ways: on the insurance arm, through reduced membership, lower revenue and higher per-member costs; and on the provider arm, through increased uncompensated care and revenue shortfalls. H.R. 1’s Medicaid financing changes—particularly restrictions on provider taxes and supplemental payments that are used to augment federal funding for the program—are projected to reduce Medicaid spending by more than $1 trillion over ten years. Hospitals alone face an estimated $665 billion in reduced Medicaid payments through 2034 and an $84 billion rise in uncompensated care costs. The downstream effects compound quickly. Reduced federal funding will pressure state Medicaid agencies to cut plan and provider rates or pursue other savings. Provider-sponsored plans will likely face margin compression as their parent health systems absorb growing charity care burdens. Safety-net hospitals under severe strain may scale back services or close—threatening plan network adequacy and care management. Even financially stable providers may push for higher commercial rates or other contractual offsets to Medicaid losses. Taken together, these pressures make careful financial planning essential for provider-sponsored plans navigating what lies ahead. |

Key Operational Recommendations for Plans

In response to these changes, plans should take action in four key areas: (1) member retention, (2) product alignment, (3) financial resiliency and (4) policy coordination. Provider-sponsored plans have some additional opportunities for action.

1) Maximize member retention within and across programs. Focus resources on preventing inappropriate disenrollments and transitioning members eligible for new programs.

- Leverage data to reduce churn: More systematically combine eligibility, enrollment, billing and engagement information to identify members at risk of Medicaid disenrollment (e.g., upcoming eligibility redetermination, subject to work reporting requirements) and Marketplace attrition (e.g., premium spike after ePTC loss, grace-period risk, need for active renewal action). Deploy analytics to prioritize outreach lists and tailor messages by language, preferred channel and prior response patterns.

- Support coverage transitions across programs: Proactively identify Medicaid members likely to shift to Marketplace coverage and provide step-by-step help (i.e., support with plan selection, verification documents and binder/first-month payment). For Marketplace members, provide clear and actionable guidance on how to re-enroll under new requirements and premium options.

- Scale customer support and systems; use AI to maximize responsiveness and efficiency: Strategically deploy tools that help to simplify notices, guide document uploads, swiftly answer routine questions and route high-risk cases to live support. Invest in capacity for predictable surges (open enrollment, redetermination peaks). Train staff on new documentation rules, extend hours as needed and improve self-service (e.g., portals, texting, upload/status tracking). Upgrade enrollment and billing systems to manage churn, movement across programs and (later) Medicaid cost-sharing. AI-enabled call triage, chatbots and intelligent routing can resolve routine questions and prioritize complex cases.

- Engage brokers and assisters: Leverage distribution channels to mitigate coverage losses. Ensure brokers, navigators and community assisters understand these changes so they can better guide consumers. Consider incentive programs for brokers who help people who are losing Medicaid coverage immediately enroll in Marketplace plans with your organization or who assist Marketplace clients through annual re‑enrollment. Emphasize cross-market continuity. Strong partnerships here can preserve membership and goodwill.

2) Align and adapt products. Rebalance offerings for higher price sensitivity (e.g., lean Bronze, narrower-network Silver). Evaluate off-exchange ACA-compliant options and ICHRA participation to retain/capture members who might otherwise drop coverage.

In Medicaid, offer targeted value-added services (e.g., transportation, nutrition supports) and deploy member engagement tactics (e.g., strategic digital touchpoints) to support care continuity, seamless re-enrollment and compliance with new program requirements.

3) Reforecast and strengthen finances. Refresh multi-year scenarios for enrollment, acuity, and rates across Medicaid and Marketplace (including work rules/redeterminations, state budget pressure and enrollment frictions). Stress-test reserves and accelerate cost control/value-based initiatives given higher acuity and rising uncompensated care risk. Rather than modeling enrollment and revenue changes in isolation by line of business, plans will need to understand how H.R. 1’s federal changes interact across Medicaid and the Marketplace and how state policy responses may amplify or mitigate those impacts.

4) Coordinate with state policymakers. Engage early on implementation to support continuity of coverage, operationally feasible compliance pathways and rates/premiums that reflect projected case-mix changes. Bring plan operations leaders into state discussions so policy design aligns with real enrollment workflows. Advocate for strong enrollment assistance and flexible consumer-support options across Medicaid and Marketplace, especially for populations with frequent eligibility transitions.

Support state use of existing data sources (e.g., wage, SNAP, tax data) to automate verification and reduce reporting burden; where appropriate, offer plan-held data to help operationalize low-friction compliance that minimizes unnecessary disenrollment.

Ongoing plan engagement in state policy development and implementation planning can help smooth the roll-out and curb rising uninsurance rates; it can also help plans gain early insight into policy decisions that will affect rates/premiums, enrollment and operations.

Additional Opportunities for Provider-Sponsored Plans

- Participate in Rural Health Transformation Fund initiatives. PSHPs serving rural areas should coordinate with states to pursue CMS’ Rural Health Transformation Fund dollars ($50B, FY 2026–2030). Prioritize investments that protect access and stabilize networks (telehealth, workforce, service-line redesign and new care models), and define measurable targets (e.g., access, quality, avoidable ED utilization).

- Integrate care management activities. PSHPs should integrate payor analytics, provider operations and clinical workflows, as feasible, to intervene earlier for rising-risk members as enrollment shrinks and acuity increases.

- Bridge payor and provider insights for policymakers. PSHPs can pair enrollment and risk analytics with provider‑side operational realities (e.g., uncompensated care growth, access bottlenecks) to help states anticipate downstream impacts on coverage continuity, network adequacy and care delivery to design more sustainable implementation approaches.

Conclusion

Plans must begin preparing for H.R. 1 now. Medicaid work requirements, increased eligibility determinations and the loss of ACA subsidy enhancements (among other changes) stand to reverse recent coverage gains and strain plan finances and operations, particularly for PSHPs, which face provider-side cost pressures as well. Impacts will vary by state and member mix, but the mission to support communities impacted by federal changes becomes ever more critical as safety-net programs contract.

Collaboration and coordination across plans, providers and policymakers will be crucial to minimizing coverage loss, ensuring member access to care and staying resilient through the change.

;

Manatt Medicaid Financing Model

Manatt Medicaid Financing Model